- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

Rodney’s Ravings: Why the market will likely lead the fall in interest rates

Guest post by Rodney Dickens

Just as the Reserve Bank waited until well after an inflation problem had developed before it started to hike the OCR, it will wait until inflation is well and truly tamed before it starts to deliver OCR cuts.

If it follows its current plan, it will keep the OCR high for far too long, just as it has in the past, causing the recession to be worse than what’s needed to tame inflation. However, if the economic fallout from high interest rates is as great as I expect, this year there should be at least a moderate, market-led fall in rates.

As you can see in the chart below, significant progress has been made in the battle against inflation, with it having fallen from a peak of 7.2% in June 2022 to 4% (grey line). This is mainly down to a decline in inflation related to internationally traded goods and services — the "tradable" component that makes up around half of the CPI — which has fallen from 8.7% to 1.6% (orange line).

Inflation in goods and services largely produced and consumed locally — a.k.a. non-tradable inflation — has fallen just 1%, from a peak of 6.8% to 5.8% (the blue line).

Tradable inflation has fallen mainly because of a drop in oil prices, but also thanks to other factors like lower residential building cost inflation. It’s normally higher than non-tradable/domestic inflation, which will need to drop to around 3% for overall CPI inflation to be back at around the midpoint of the Reserve Bank’s 1-3% target range.

The Reserve Bank predicts that non-tradable inflation should reach 3% by March 2025 (shown as the grey line in the second chart, below) although it didn’t fall as much as was expected in the recent March quarter. It’s also predicting that the OCR won’t start to fall until significantly later than this (blue line).

![]()

Waiting to cut the OCR until after underlying inflation is fixed is as misguided as waiting until non-tradable inflation had reached 4% before starting to hike (which the Reserve Bank also did). If it does this it will inflict more pain than needed to tame inflation, just as it allowed inflation to become somewhat entrenched before it started to hike.

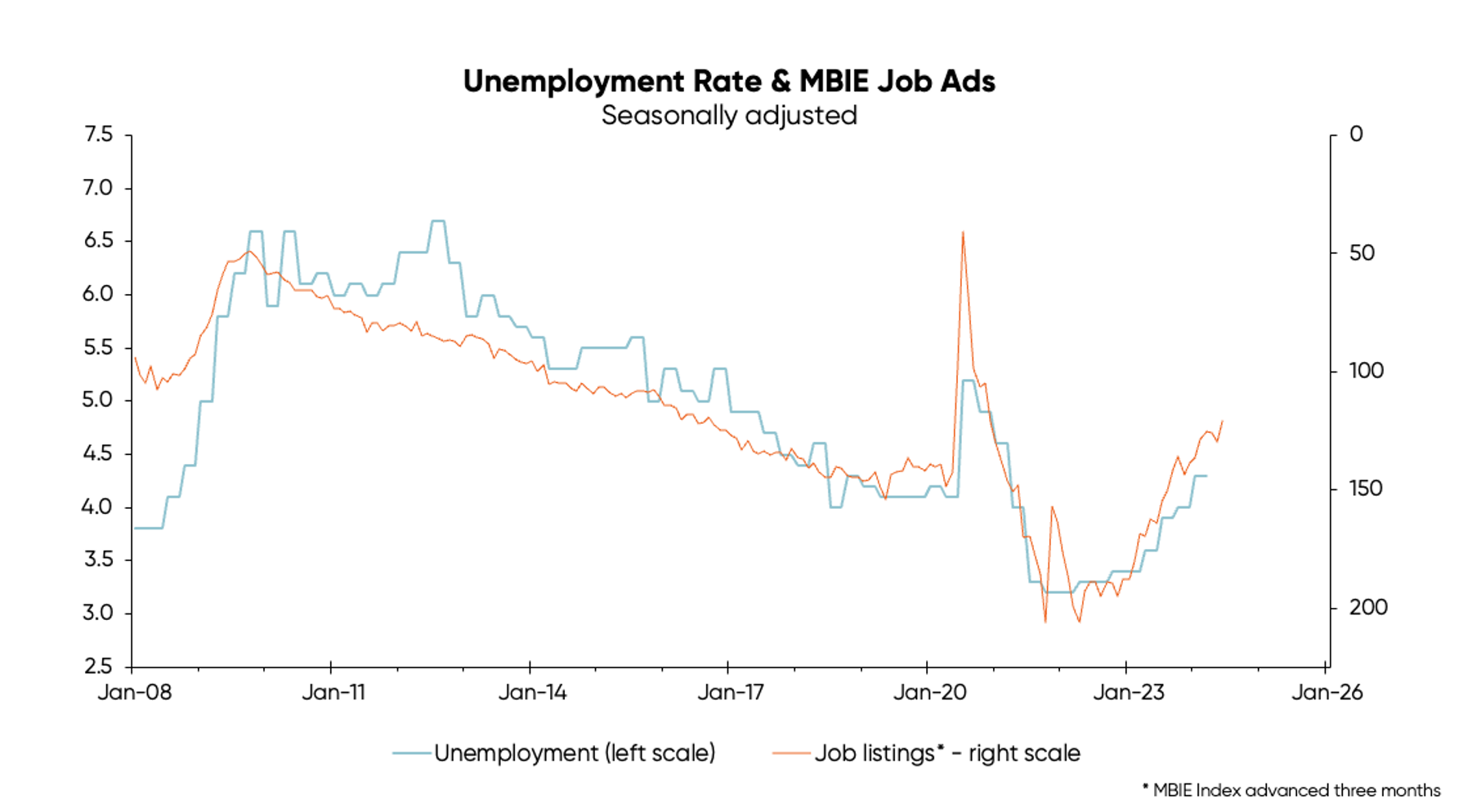

Evidence the Reserve Bank has probably already done enough to tame inflation can be seen in the large fall in job listings, which is a reasonably useful leading indicator of the unemployment rate (illustrated in the third chart). Job ads are also a useful leading indicator of capital spending that has started to fall more than the Reserve Bank is predicting and plays a critical role in economic upturns and downturns.

Unfortunately, the Reserve Bank has a tradition of being too slow to hike and cut and is likely to continue this tradition because of its poor forecasting and lack of understanding of what is going on at the coalface of the economy.

However, the market is usually quicker to respond. If economic growth deteriorates as much as leading indicators like job ads suggest, implying significant progress will be made in getting non-tradable inflation down this year, the market should start to front run a fall in interest rates.

Consistent with this, medium and longer-term wholesale interest rates (swap rates) have already fallen below the OCR — as shown below in the fourth chart.

![]()

If economic growth continues to be weaker than the Reserve Bank predicts, the market should be more inclined to lead the fall in interest rates and the Reserve Bank should be less inclined to lean against a market-led fall.

It's a pity the Reserve Bank doesn’t make proactive versus super-reactive OCR decisions although the silver lining is that the more it overdoes the unfolding recession the greater the chance for reasonably sustained economic and housing upturns thereafter.

By Rodney Dickens, Managing Director, Strategic Risk Analysis Ltd www.sra.co.nz.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.