- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

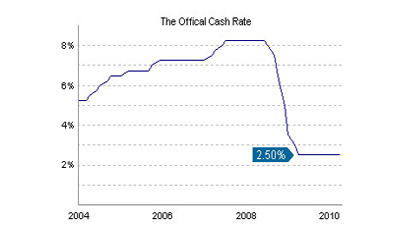

Mortgage rates | OCR unchanged at 2.50%

As expected the official cash rate (OCR) remained unchanged today. Better still, Big Al (the "Gov") left the door open to not start pushing rates up until later in the year. I think he will be quietly happy with the way things are going.

My perspective is that our Reserve Bank is doing a great job. I'm especially glad to see them not knee-jerking when our economic recovery is still VERY fragile. The way I see it ... exports are improving helped by a strong Aussie dollar and consumer spending is still subdued. Meantime low interest rates are helping us slowly deleverage and there is less money leaving the country as interest payments. This is all positive so let’s have more of the same. Banks are still tight on lending and Government reform in the budget should help rebalance the economy putting less pressure on interest rates. We also have around 30% of our mortgage market on floating rates and another 30% on short-term fixed rates. When rates do eventually increase, the impact on the economy will be quick, and as such Big AL will not need to move interest rates much at all.

So should I fix or float?

My view has not changed – stick with short-term rates even when rates do eventually start to increase. I'm starting to get bored of repeating the same mantra ... an interest rate at a point in time is irrelevant ... it is how interest rates perform over time (or your total interest costs) that really matters. Our whole psychology around fixing is completely wrong. Have a play with our rate forecaster to help you figure out the right strategy. [download id="5711"] Personally I’m splitting my hefty mortgage between floating and 18-month fixed rates. I think all rates from floating to 18-month fixed rates offer great value. The two-year rate and longer-term fixed rates are still overpriced relative to where mortgage rates will go over the next few years. I’d be happy putting everything on floating, but given my indifference between floating and the 18-month rate, I’m happy to split across both and reduce any residual uncertainty. Whilst the 18-month rate is higher than floating, once you factor in rising rates over the next 18 months the total interest cost of both options is about the same. We Kiwis have a psychological aversion to putting everything on floating. But who cares? If splitting 50/50 or even 33/33/33 helps you sleep better at night then go for it. There is no one right answer!

Your banker is not a guru

Not surprisingly I have had a number of people tell me that mortgage rates will fall. Digging deeper, it seems to be coming from "my friend that works in the bank." I won't dig into the logic only to say it is fundamentally flawed. If you haven't figured it out yet, getting interest rate advice from a retail banker is no different to getting financial advice from your taxi driver. Bank staff are trained to provide great service (mostly), sell you lots of stuff, and use computers. They are not trained to give advice and they are not impartial. One thing is for sure... mortgage rates will not fall and when rates do start to increase you won't pick it fast enough. My advice? Don’t try to second-guess the market. Have a game plan and stick to it. If your intention is to eventually fix, then you might as well fix your mortgage now.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.