- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

Buying and building new

When it comes to building new there are a few different types of construction contracts available and it's important you pick the right one for you.

We're here to help.

Start an application Book a chat

Deconstructing construction lending

Our job is to make the whole process simple and save you money. Our team of mortgage brokers will give you personal, unbiased advice. And you’ll get a great rate too.

We’ll chat about what you’re wanting to achieve, provide expert advice and guide you through the process, then approach the right lender for your situation to get you the best deal.

Get the guide to buying a new build sent to your inbox

Buying off plan

Before you get down to business, you’ll want to get clued up on how buying one of these sites actually works.

Buying off-plan is a bit different to when you can physically eye up your new home. It requires a small leap of faith. You’re buying something sight unseen with a few artist impressions and written specifications to fill the void. The benefit is that they are often better value-for-money and you don’t need to fight it out each week at auctions. The challenge is getting your head around what you’re buying.

The other advantage is the deposit amount. We all know that saving for a big enough deposit to get you into the Auckland market is the biggest hurdle, but there are more lenient rules around lending for off-plan homes, and you don’t have to have a 20% deposit like you would if you were buying an existing house.

Have a look at the different types of loans you can get below, as well as the various payment structures.

Turn Key Contract

This type of construction loan is beneficial to the client, but it can make it harder for the builders. That's because a turn key contract is essentially a fixed price contract between you and the builder that specifies a fully completed property or renovation, including landscaping, driveways, painting and flooring in the new property.

Things to note:

A turn key contract only allows for minimal ‘PC Sum’ (non-fixed) costs, meaning that the costs shouldn’t blow out once construction is underway.

This contract is exempt from RBNZ (Reserve Bank of NZ) rules. That means you don’t need a 20% deposit - a 10% deposit (20% for investment properties) is required for turn key contracts, and some banks may even stretch to allow 5% in special circumstances, making this an attractive option for those with good income but less savings.

Another advantage to you the client is that until the property has been completed and settled, you don’t make any loan repayments or pay any interest, allowing you additional time to save before you start to pay off the loan.

Land and Build Contract

This is the most common type of construction loan and builders love this type of contract.

Like the turn key, it specifies completion of a ready to live in building with minimal ‘PC Sum’ costs.

Again, like turn key, these loans are exempt from RBNZ policies and therefore banks only require a 20% deposit if it’s an investment property (10% deposit is fine for first home buyers). The big difference is that there are progress payments involved. These progress payments are funds that go to the builder at various stages of the project (outlined in the table). Think of it as a 'pay as you go' approach. You start paying interest on your loan as soon as the first payment is made - which is typically at settlement of the land - and your loan payment increases as each new payment is made.

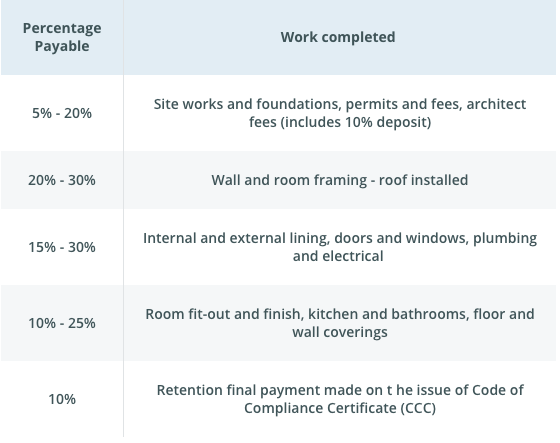

Progress payments

Firstly, a 10% deposit will be required to secure the contract. This is then included in the first drawdown. Normally paid by cash or equity.

The second drawdown tends to be 20% of the total balance of the build contract.

To give you an idea of how the entire payments might typically pan out, the rules of thumb shown in this table can be used.

Labour Only/Partial Contract

We wouldn’t recommend you sign one of these bad boys unless you’re relatively experienced in construction contracting and how it all works.

These contracts come in many forms but normally consist of a range of sub-contracts that are managed by either the client or a project manager. There might also be a labour only arrangement with the contractor.

These types of contracts are commonly used in the case of a kitset or relocatable home.

Lending for a labour only or partial contract is limited to the land value only unless the buildings are already permanently fixed to the land. LVR would typically be between 65% - 80% depending on the contract. The bank will also include a 10% - 20% contingency as these loans almost always go over budget.

Other conditions for labour only / partial contracts:

- Quotes for materials and subcontractors required up front

- Progressive drawdowns are made against invoices

- Valuations for each drawdown stage are required to ensure any cost blowouts are identified early

Conditions

Not only does buying off the plan require a small leap of faith, it also comes with a whole heap of other lending conditions. Here are some typical conditions to expect in a build loan approval:

- Sales and Purchase of the land (or the full purchase price if you are going with the turn-key option)

- Fixed price Master Builders contract

- Building/resource consent

- Registered valuation showing the value 'as is' and 'on completion'. Depending on the bank, you may need an updated valuation at each staged payment and again on completion, or you may just need a completion certificate.

So get in touch with one of our advisers today.

More banks, more choices

Plus a network of over 5,000 peer-to-peer lenders

Not only do we have access to more banks than other brokers, but we have a community of over 5,000 peer-to-peer lenders for a custom solution if you don't quite fit the bank's box.

We've settled over $20 billion in mortgages. And because we're always scouring the market for a better deal, you can count on us to drag more money out of those fat cats.

Anonymous

New Zealand

Really happy Basil was amazing, very efficient, great communication and he worked with us to get a good result. Would recommend him to others[N

Luke Murray

New Zealand

It was a great experience. The refinance helped me greatly and put me in a position to keep my apartmentLM

Ryan

New Zealand

The service I got from Squirrel was extremely efficient. They dealt with my loan so easily and achieved a result greater than what I was expectingR

William

New zealand

Sudam our advisor was so helpful, patient and knowledgeable and made the whole process super easy with a great final resultW

Ryan Grant

New Zealand

Alex McRobbie was awesome! Informed knowledgeable and understanding! best outcome and awesome person to deal with! Couldnt recommend highly enoughRG

Martin

New Zealand

Helped me get an improved rate and sorted out my needs. Great communication, kept me up to date throughout the process.M

Dan Clark

New Zealand

Kat McInnes was so helpful and a pleasure to deal with.Kat made the whole experience less stressful and so straight forward. I would have no hesitation in recommending Kat to anyone who needs any help with Mortgage lending.DC

Denoa Amoa

New Zealand

Eleanor was very communicative, explained to me the best options and structure available, and guided us through what was a complicated process due to the structure of the ownership.DA